Section 73 vs Section 74 in CGST: Litigation Trends & Rulings

Understand the difference between Section 73 and Section 74 of CGST Act, penalties, time limits, and latest GST litigation trends.

Understand the difference between Section 73 and Section 74 of CGST Act, penalties, time limits, and latest GST litigation trends.

If there is one issue that repeatedly triggers GST litigation in India, it is the wrong invocation of Section 74 instead of Section 73.

Almost every taxpayer who receives a show cause notice under Section 74 of the CGST Act asks the same question:

“Is this really a fraud case, or is the department stretching it?”

The distinction between Section 73 and Section 74 is not just technical. It directly affects:

Courts across India have repeatedly held that Section 74 cannot be invoked casually. Yet, in practice, GST notices often allege suppression of facts or wilful misstatement without proper reasoning.

This is precisely why early legal evaluation matters. A seasoned tax consultant in Gurgaon can often identify, at the notice stage itself, whether the department has wrongly invoked Section 74 and whether the case legally falls within Section 73.

This article breaks down Section 73 vs Section 74, explains how litigation is evolving, and highlights key judicial trends every taxpayer should be aware of.

The CGST Act, 2017 provides two separate tracks for recovery of tax that is:

These tracks are governed by Section 73 and Section 74 of the CGST Act.

The entire scheme depends on intent.

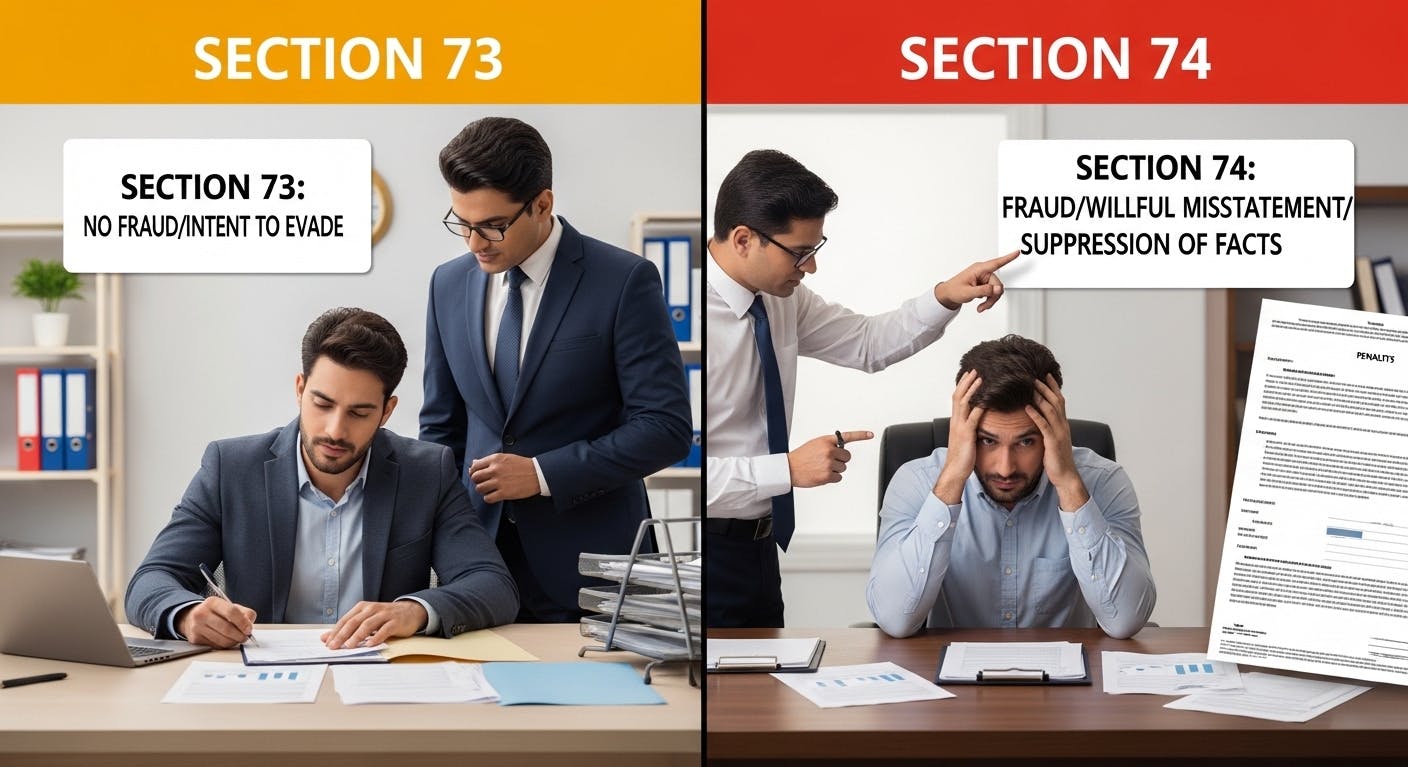

Section 73 of the CGST Act applies when tax is not paid, short paid, or ITC is wrongly availed for reasons other than fraud, such as:

There is no allegation of intent to evade tax.

In simple words:

Section 73 is for errors, not deception.

Courts have repeatedly held that mere discrepancy does not amount to suppression of facts.

This is why taxpayers strongly contest wrongful invocation of Section 74.

Time limits are strictly interpreted by courts.

Know more: How to Deal with GST Show Cause Notices (SCNs) Practical Guidance for Businesses

Section 74 of CGST Act applies when non-payment or short payment of tax is due to:

This is the penal provision of GST law.

Courts have clarified:

Mere failure to disclose information when records are available does not amount to suppression.

This makes Section 74 extremely costly for taxpayers.

Because of this extended limitation, Section 74 is often misused.

In recent years, GST officers increasingly issue notices under Section 74 even for:

The reason is simple:

However, courts have started pushing back.

Courts have consistently held:

Allegation of fraud cannot be mechanical.

The proper officer must demonstrate:

High Courts have repeatedly observed that Section 74 cannot be invoked merely because tax is short-paid or ITC is disputed. There must be tangible material showing deliberate wrongdoing. In fact, courts have gone on record to clarify that Section 74 cannot be invoked mechanically without evidence of fraud.

This evolving judicial approach has made early legal scrutiny crucial. A knowledgeable gst consultant in gurgaon can assess whether a Section 74 notice is legally sustainable or vulnerable to challenge, often preventing prolonged and unnecessary litigation.

Without such evidence, Section 74 notices fail and are routinely struck down as arbitrary and unsustainable in law.

Failure to pay tax by itself does not justify Section 74.

If:

Then suppression cannot be alleged.

Courts protect taxpayers where:

In Section 74 proceedings:

Recommended: GST Limitation Period Explained: Notices, Appeals & Deadlines Before March 31, 2026

Such notices are routinely challenged.

Courts insist on:

Mechanical confirmation of tax and penalty is struck down.

One of the most litigated areas is ITC wrongly availed.

Courts have clarified:

Erroneous refund cases are often wrongly tagged as fraud.

Judicial view:

During adjudication:

Orders merely repeating notice language do not survive appeal.

Paying tax:

This is critical in Section 74 cases.

Successful appeals often argue:

Many Section 74 orders are converted into Section 73 by appellate authorities.

To sustain Section 74, department must establish:

Failure on any count weakens the case.

The distinction between Section 73 and Section 74 of the CGST Act is not academic it is the backbone of GST litigation.

Courts are clear:

For taxpayers, understanding this difference can:

Given the overlap between GST disputes and direct tax compliance, coordinated advice becomes critical. Many businesses rely on an experienced income tax consultant gurgaon to evaluate intent, documentation, and risk exposure across tax laws, ensuring that allegations of fraud are challenged at the right stage.

In GST, intent matters as much as tax.

Understand GST on export vs intermediary services, key differences, recent rulings, and litigation risks. Avoid disputes with this practical 2026 guide.

Understand the latest 2026 judicial trends in India’s cross-border taxation and how key court decisions affect global tax strategies.

Learn how to optimize tax on cross-border royalty & FTS payments under DTAA. DSRV India explains GST implications, TDS rules & smart compliance strategies.